The question has moved from fringe financial blogs to the boardrooms of Fortune 500 companies and the pages of peer-reviewed academic journals. Researchers at MIT, Stanford, the Brookings Institution, and the National Bureau of Economic Research (NBER) are all producing serious work on the same topic: is the current wave of AI investment sustainable, or are we watching history repeat itself?

The honest answer is that nobody knows for certain. What we do know is that the evidence on both sides of the debate is compelling — and that the outcome matters enormously for every business that is building its strategy around AI right now.

The case that a bubble exists

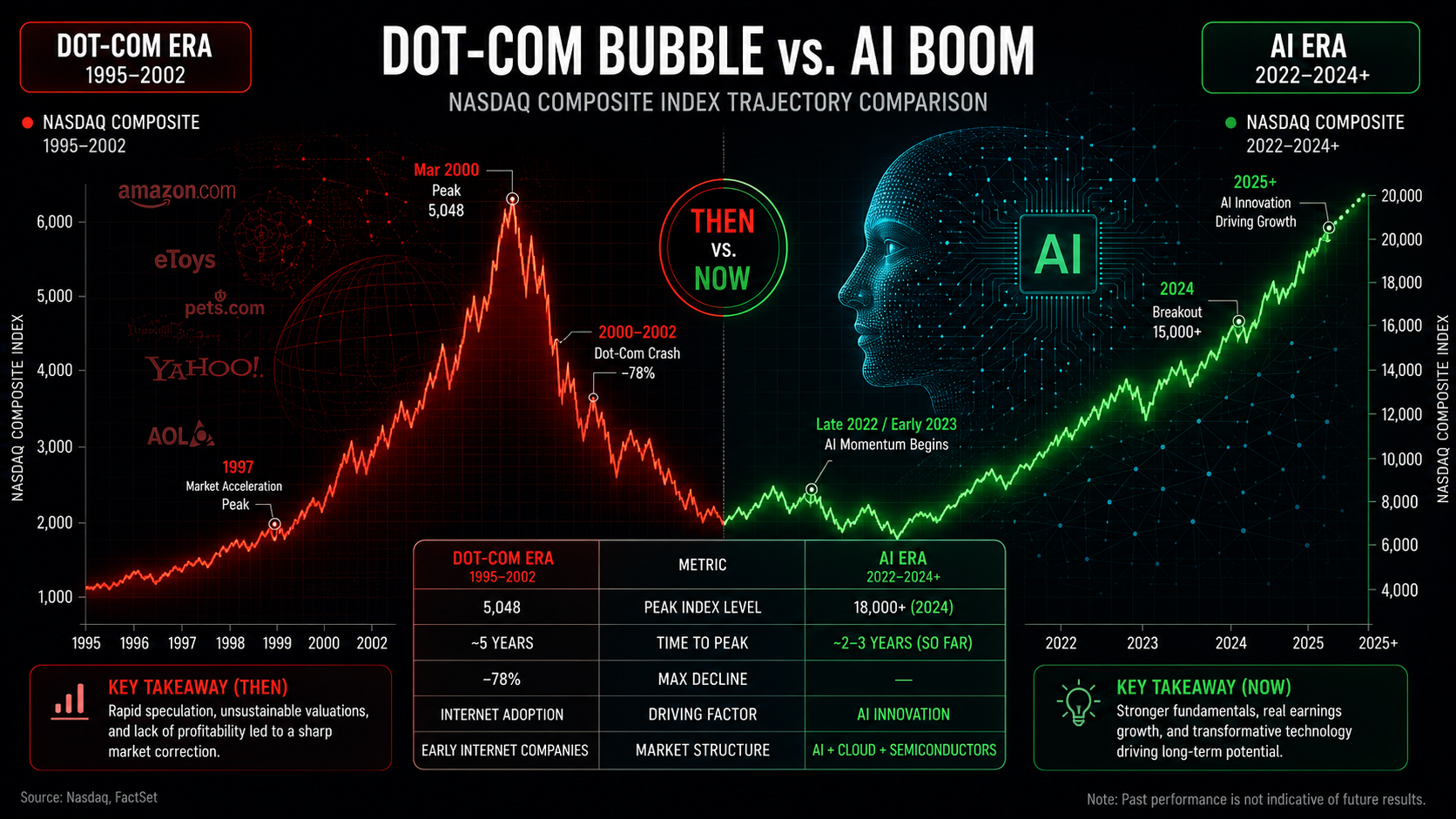

The numbers are staggering. According to the Brookings Institution’s senior fellow Darrell West, the scale of current AI investment is almost without precedent. Amazon is devoting $100 billion to data centers in 2025 alone. Meta has committed over $600 billion across the next three years. Microsoft planned $80 billion for the same timeframe, and Google pledged $75 billion. Apple is planning $500 billion in technology expenditures — including AI — over the next four years. As West notes, AI investments are now running into the trillions in actual or planned expenditures.

The concern is not that AI lacks potential. It’s that the money is flowing in far faster than the revenues justify. MIT Sloan professor Gary Gensler — a former SEC chair — has noted directly the gap between AI spending and AI revenues. Capital expenditures on data centers and AI infrastructure reached $400 billion in 2025 and are expected to approach $500 to $600 billion in 2026. The revenue directly generated by generative AI products, by contrast, represents only a fraction of that figure.

Thomas Davenport and Randy Bean, writing in the MIT Sloan Management Review, put it plainly: the sky-high valuations of AI startups, the emphasis on user growth over profits, the intense media hype, and the expensive infrastructure buildout all bear uncomfortable similarities to the lead-up to the dot-com crash of 2000. “It’s hard not to see the similarities,” they write. “The AI industry and the world at large would probably benefit from a small, slow leak in the bubble.”

Stanford HAI co-director James Landay has been even more direct, stating in Stanford’s 2026 predictions: “At some point, you can’t tie up all the money in the world on this one thing. It seems like a very speculative bubble.”

Adding economic rigor to the debate, Harvard and MIT economist Ricardo Caballero published a working paper through the NBER titled “Speculative Growth and the AI Bubble” in early 2026. His analysis explores how AI technology can generate “speculative-growth equilibria” — conditions where high valuations and massive investment are mutually self-reinforcing, but where the mechanism is inherently fragile. As Caballero’s framework concludes, a loss of confidence can trigger a self-fulfilling crash and reversal. The structure of the current moment, in other words, has the mathematical properties of a bubble — whether or not one ultimately materializes.

The productivity paradox: where are the results?

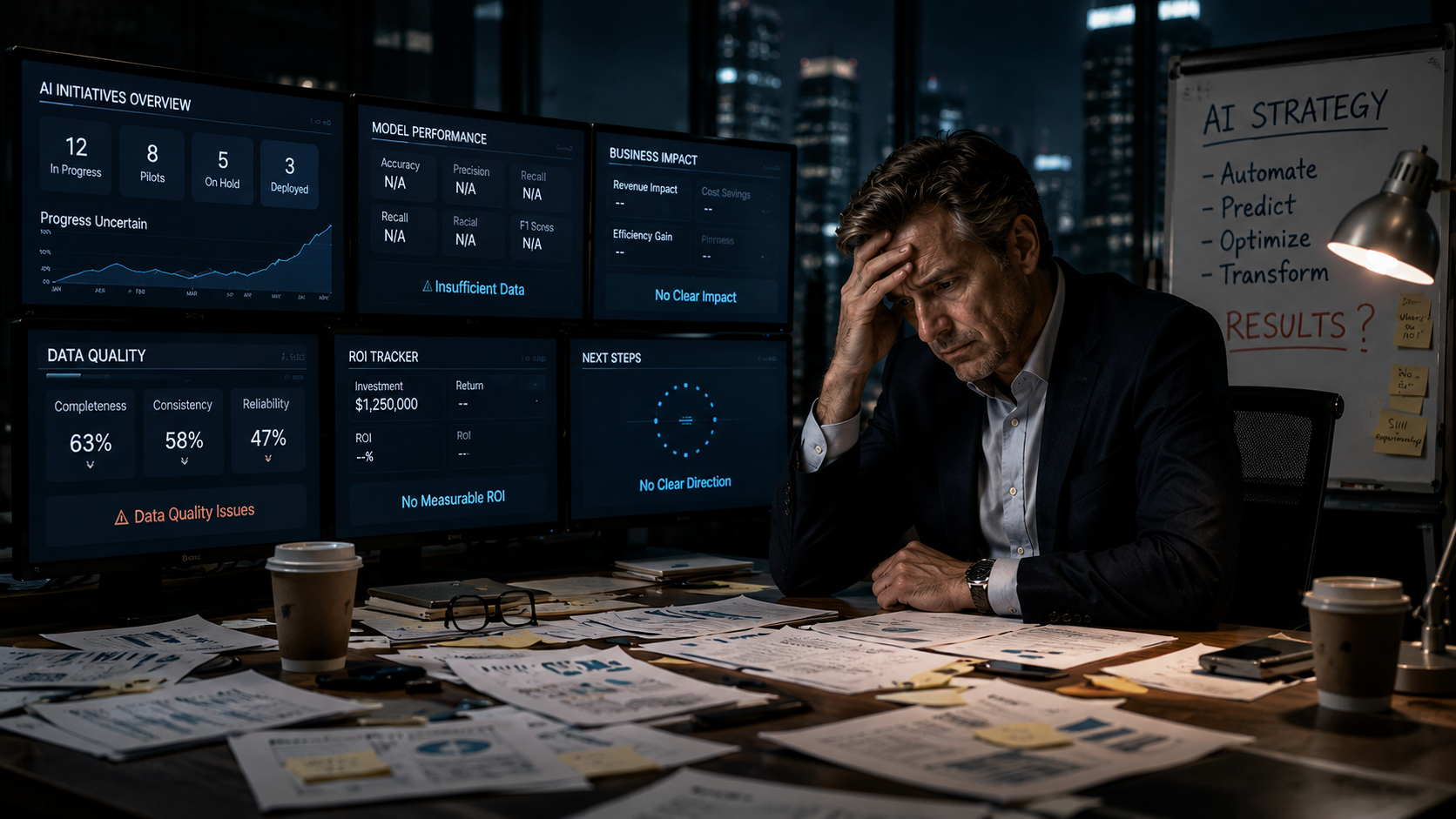

Perhaps the most striking piece of evidence in the bubble debate is not about money at all. It’s about what businesses are actually experiencing on the ground.

A large-scale NBER survey of nearly 6,000 senior business executives across the U.S., U.K., Germany, and Australia found that while 69% of firms actively use AI, nine in ten executives reported no measurable impact on employment or productivity over the previous three years. To put that in perspective: three years of widespread AI adoption, accompanied by trillions in investment, and the majority of businesses cannot yet point to a clear, measurable return.

Executives report no measurable impact of AI on employment or productivity over the past three years, despite widespread adoption. (Source: NBER, 2026)

Economists have a name for this pattern. It echoes the “productivity paradox” of the 1980s and 1990s, when personal computers were spreading rapidly across offices but economic productivity statistics showed no corresponding gains. The computers were there. The impact took a decade to show up. Stanford researchers and MIT Sloan economists are now watching carefully to see whether AI follows the same delayed-payoff pattern — or whether the productivity gains simply never arrive at the scale the valuations require.

Stanford’s 2026 AI expert predictions reinforce this picture. Multiple faculty members across computer science, economics, and medicine converge on the same observation: 2026 is the year companies will begin openly saying that AI has not yet delivered the broad productivity increases that were promised. “We’ll hear about a lot of failed AI projects,” noted one Stanford HAI faculty member. The era of AI evangelism, Stanford’s researchers conclude, is giving way to an era of AI evaluation.

The case that this is not a bubble

For every data point suggesting overvaluation, there is a serious counterargument — and it deserves equal attention.

The Stanford HAI 2026 AI Index Report — one of the most comprehensive annual assessments of AI progress — documents genuine and accelerating capability gains. Industry produced over 90% of notable frontier models in 2025, and several of those models now meet or exceed human baselines on PhD-level science questions and multimodal reasoning tasks. Generative AI reached 53% population adoption within three years — faster than the personal computer or the internet. The estimated value of generative AI tools to U.S. consumers alone reached $172 billion annually by early 2026, with the median value per user tripling between 2025 and 2026.

Estimated annual value of generative AI tools to U.S. consumers by early 2026 — with median value per user tripling in just one year. (Source: Stanford HAI 2026 AI Index)

Private AI investment in the U.S. reached $285.9 billion in 2025 — more than 23 times the investment level seen just a few years prior. That is not a small market finding its footing. That is a technology reshaping entire industries in real time.

Randy Bean, in his MIT Sloan commentary, offered a framing that cuts through the short-term debate: “Often technologies are overestimated in the short term, but their transformational impact is very much underestimated in the long term.” The companies that dismissed the internet in 1997 because the dot-com bubble looked inflated missed one of the greatest economic transformations in history. The productivity gains from the internet were real — they just arrived on the internet’s schedule, not the market’s.

Caballero’s NBER working paper, despite identifying the speculative properties of the current moment, also leaves open the possibility of a “high-capital outcome” — a scenario where the investment boom is self-sustaining because AI’s labor-substituting properties continuously expand productive capacity. In other words, the mathematical conditions for a soft landing exist alongside the conditions for a crash. Which scenario materializes depends on whether AI adoption and revenue catch up to valuations before confidence erodes.

The six warning signs to watch

Darrell West at the Brookings Institution identified six key indicators that analysts and business leaders should monitor to assess bubble risk in real time. Understanding these factors won’t let you predict a crash — but they give you a structured way to read the signals as they emerge.

Six bubble risk indicators to monitor

- AI investment levels — when spending on infrastructure grows faster than revenue, the gap becomes a risk indicator

- Data center construction timelines — construction outpacing demand signals overextension

- AI adoption levels — plateauing adoption rates would be an early warning sign for inflated valuations

- Price of AI products — aggressive price competition (as seen with low-cost Chinese models) can compress margins

- Company competition — a hyper-competitive market with rapidly commoditizing models puts pressure on market leaders

- Public trust in technology — documented AI incidents rose to 362 in 2025, up from 233 the prior year (Stanford HAI)

What this means for your business right now

Whether the bubble pops or deflates slowly or simply never bursts, the strategic implication for business owners is the same: the window to build genuine, measurable value from AI is now — not later.

The businesses that win in either scenario are not the ones that spent the most on AI. They are the ones that deployed AI against specific, measurable problems and built internal processes around the tools. The NBER survey’s finding that nine in ten executives saw no productivity impact is not an argument against AI — it is an argument against using AI without a clear strategy. The 10% of businesses that do report meaningful productivity gains share a common trait: they implemented AI in focused, outcome-oriented ways rather than as a general-purpose experiment.

The Brookings Institution’s framework for bubble risk monitoring is also directly applicable to business decision-making. Rather than betting everything on AI tools staying at current prices, businesses should build workflows that deliver value today, at current pricing, and remain adaptable as the landscape shifts. If model prices drop due to competition — or rise due to consolidation — a well-designed AI workflow should be adjustable without requiring a complete rebuild.

MIT Sloan’s guidance for AI decision-makers in 2026 is pragmatic: take full advantage of the AI technologies already available while also building a clear-eyed view of what AI investments can realistically deliver for your specific business model. The companies sitting on the sidelines waiting for certainty will find themselves years behind. The companies over-investing in AI without measurable outcomes may find their strategies unsustainable if valuations correct. The path is in between: deploy with purpose, measure relentlessly, and build on what works.

The bottom line

The AI bubble debate is not a reason to stop investing in AI. It is a reason to invest smarter.

The technology is real. The capability gains documented by Stanford HAI are real. The consumer value is real. What is uncertain is whether the current market valuations — and the infrastructure spending behind them — are proportionate to the pace at which revenues will actually materialize.

For business owners, that distinction matters less than it does for Wall Street. You are not buying AI stocks. You are deciding whether to deploy AI tools that save your team time, improve your customer experience, and help you compete against businesses ten times your size. On those terms, the calculus is clear. The risk is not that AI stops working. The risk is that you wait too long to use it.

The businesses that emerge strongest from this moment — bubble or not — will be the ones that were building while others were debating.

Sources

- West, Darrell M. Is there an AI bubble? Brookings Institution, Center for Technology Innovation. November 2025. brookings.edu

- Davenport, Thomas H. and Randy Bean. Five Trends in AI and Data Science for 2026. MIT Sloan Management Review. January 2026. sloanreview.mit.edu

- Action items for AI decision makers in 2026. MIT Sloan. March 2026. mitsloan.mit.edu

- Gensler, Gary. The Fed, AI, and economic uncertainty: What investors need to know. MIT Sloan. April 2026. mitsloan.mit.edu

- Caballero, Ricardo J. Speculative Growth and the AI “Bubble.” NBER Working Paper 34722. January 2026. nber.org

- Yotzov, Ivan et al. Firm Data on AI. NBER Working Paper 34836. February 2026. nber.org

- Stanford AI Experts Predict What Will Happen in 2026. Stanford HAI. December 2025. hai.stanford.edu

- The 2026 AI Index Report. Stanford HAI. April 2026. hai.stanford.edu

Ready to deploy AI with purpose?

Double O Digital builds AI assistants for local businesses that deliver measurable results — not just demos. Let’s talk about what’s right for yours.

Get Started →